In the United States we have enjoyed the largest economy in the world for so long that we often don't think of how events around the globe affect us. Maybe we just don't want to admit that we are suceptable to the economic occurances that take place twelve thousand miles away in some small country! But those things do affect us now that we really operate in a global economy and the macro view is not just a look at the United States any more - it is a look at the world. Maybe we will have to reference Macro as the Super Macro View for the world economy, vs. the Macro View for the U.S. Economy. Luckly we have not sneezed this year so the rest of the world has not caught a cold, but there are events that have occured that are affecting us. Maybe what we have is a case of "the argues" as old Festus from Gunsmoke use to describe his aches or pains in his body - it was when one part of the body was arguing with the other! (Wow that really dates me!)

Macro Overview

Macro risks are still prevalent throughout the world as the effects of Brexit and terrorism continue to be ongoing concerns. U.S. markets have been resilient to the uncertainties, as major U.S. stock indices reached new highs in July.

Some believe that the outcome of the EU vote, as well as the sentiment in Britain shortly before the vote to leave the EU, has many similarities to the U.S. presidential race. Key election issues and how they may affect the economy include: NAFTA, immigration, terrorism, and banking regulations such as Glass-Steagall and Dodd-Frank.

The presidential campaign has brought about the suggestion of reforming existing regulations, which are adversely affecting the banking and financial services industry. Some candidates argue for the repeal of Dodd-Frank, regulations put in place during the current administration to regulate banking activity.

The problem has been that the costs of the new regulations have inhibited smaller banks and credit unions. Some candidates lobbied to bring back legislation known as Glass-Steagall, put in place during the depression in order to prevent banks from combining financial services and lending simultaneously with the more risky business of investment banking.

In the last eight years since the “Great Recession” there have only been four community banks started in all 50 states, down from about 160 in 2007. Community banks are often a major economic engine for the local economies.

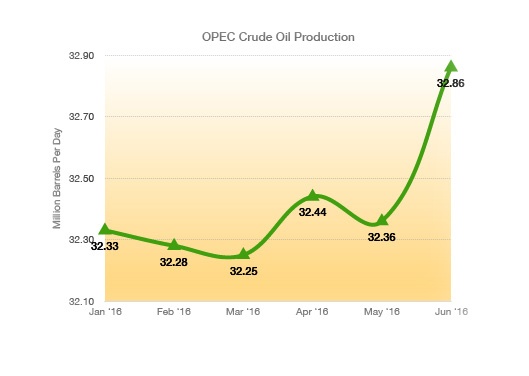

Economic growth, measured as GDP, was reported by the U.S. Department of Commerce to have increased at an annual rate of 1.2 % in the second quarter of 2016, below analyst’s expectations of 2.5%. The dismal GDP report was accompanied by a drop in oil prices of over 15% in July and a record low for the 10-year Treasury yield hitting 1.37%.

Upcoming economic data for the U.S. may influence the Federal Reserve to act on raising rates rather than waiting any longer. Analysts believe that a rate increase by the Fed before the end of 2016 based on U.S. economic data may be a mistake. Rates in Europe and Japan remain in negative territory due to the uncertainty of growth within the EU and the expected derogatory effects of Brexit on global business transactions. Fed members decided to leave interest rates unchanged during their July meeting, stating that it was prudent to wait for more data following the consequences of Britain leaving the EU.

Banks in Italy have become the latest of concerns in Europe as souring loans are being recognized throughout the Italian banking sector. As the third largest economy in the EU, Italy’s banking sector is prone to a crisis that could have dire consequences for the country and neighboring trading partners.

Stagflation On The Horizon – Monetary Policy

Former Fed Chairman Alan Greenspan said that the U.S. may be heading toward stagflation, a slow-growth economy coupled with rising inflationary pressures. Greenspan also said that there seems to be pockets of inflation even though low productivity is prevalent in the economy.

Stagflation is an economic phenomenon when there is slow or stagnant economic growth at the same time as rising inflationary pressures. The 70’s were a period when rapidly rising fuel prices coupled with dismal economic growth, led to stagflation. This same scenario occurred in the first two years of the 80’s, until both monetary and fiscal policies were enacted that halted destructive inflationary pressures and curtailed taxes to boost economic activity.

Inflation is measured by the CPI (Consumer Price Index) and economic growth is gauged by GDP (Gross Domestic Product), which are both released by the Department of Commerce each month. As a barometer of general prices throughout the country as well as current economic activity, both indices help identify any possible stagflation scenarios.

Managing your way through this current economic time can be challenging. It would seem that rates will remain low for the near future, certainly into 2017. The Fed may make minor adjustments, but I don’t think we will see any drastic increases. Wall Street needs better earnings to keep it going, I think they have had their fill of low rates. It’s a good time to review where you are at, and how your plans are shaping up for the year. Additionally, now is the time to start the final work for income tax reduction strategies, as we finish the third quarter. It much better to do this now rather than starting in December!

The current low rate environment, is no longer an effort to keep fueling Wall Street, but in an effort to keep the Federal Government afloat (they are the largest borrower in the world). If rates increase for the government, then ALL TAXES must go up to pay for the increases in interest payments. Don’t get me wrong, lower rates do help the Market, but the Market has adpted to lower rates for some time. Now the Federal Government needs to get its borrowing under control for the rest of the economy to move forward. (See Feed the Pig Article)

Sources: EuroStat, Dept. of Commerce, BEA, Federal Reserve, ECB

Remember:

"So that the record of history is absolutely crystal clear. That there is no alternative way, so far discovered, of improving the lot of the ordinary people that can hold a candle to the productive activities that are unleashed by a free enterprise system." Milton Friedman