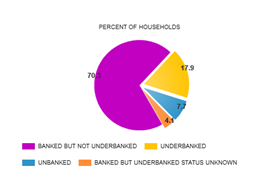

For marijuana growers and retailers in the states that have legalized the drug for recreational or medical use, money and banking are perhaps the most vexing challenges of doing business. Piles of cash accumulate in back rooms and safes, making the businesses, their employees and their customers a target for robberies. Businesses often have no access to business loans or regular lines of credit. Many say they struggle to even keep a checking account open to pay their employees or electricity bills.

Legal sales of marijuana have already reached $2.6 billion so far this year. Most estimates predict sales from medical marijuana will likely reach $3 billion by the end of 2014, up from $1.5 billion in 2013. Marijuana can be grown legally in 23 states and the District of Columbia; and another 11 states have limited legal access, often for research purposes, according to the National Conference of State Legislatures. A recent Huffington Post article cited studies that predict that legal marijuana sales could bring in between $7.4 and $8.2 billion in revenue by the year 2018.

Source: ProCon.org

Under federal statues, the use, possession, sale, cultivation, and transportation of cannabis (marijuana) in the United States under federal law is illegal but the federal government has announced that if a state wants to pass a law to decriminalize cannabis for recreational or medical use they can do so, but they need to have a regulation system in place for cannabis. Cannabis is listed as a Schedule I substance under the Controller Substances Act of 1970, the highest classification under the legislation. This means that the substance has been decided by the federal government to have both high abuse potential and no established safe medical use.

However the stimulation or boost, selling and taxing marijuana will provide to both the state and national economies has become very evident to lawmakers. Take the state of Colorado that has implemented selling recreational marijuana. On the first day of 2014 alone, shops opened across the state totaled over $1 million in sales, according to multiple sources. Combine that with a nearly 29 percent tax rate statewide, and you can calculate what the state is anticipating in revenue. The Colorado State Department of Revenue reported that as of July 2014, the state sold $29.7 million worth of recreational marijuana which was slightly higher than $28.9 million worth of medical marijuana sold in the same month.

In January, 2014, Attorney General Eric H. Holder Jr. stated, “that lawful marijuana businesses should have access to the American banking system and that the government would soon offer rules to help them gain it. The rules are not expected to give banks a green light to accept deposits and provide other services, but would tell prosecutors not to prioritize cases involving legal marijuana businesses that use banks. “You don’t want just huge amounts of cash in these places. They want to be able to use the banking system,” Mr. Holder said at the Miller Center at the University of Virginia. “There’s a public safety component to this. Huge amounts of cash, substantial amounts of cash just kind of lying around with no place for it to be appropriately deposited, is something that would worry me, just from a law enforcement perspective.”

While marijuana is illegal in most states and is prohibited under federal law, the Obama administration said last summer that it would allow Colorado and Washington State to move ahead with legalizing the drug for recreational use. In an interview with The New Yorker, President Obama said that despite his misgivings about marijuana and the push for broader legalization of the drug, it was important that Colorado’s and Washington’s experiments go forward. “It’s important for society not to have a situation in which a large portion of people have at one time or another broken the law and only a select few get punished,” he said.

A bipartisan effort to help marijuana entrepreneurs is emerging. The House amendment passed July 16th (HR5016) that should help marijuana businesses get banking services in the 23 states where marijuana is legal in some form. Specifically, the amendment prohibits the Treasury Department from spending money to penalize financial institutions that serve legal marijuana businesses. It passed 231 to 192.

Last May, the House passed another appropriations bill amendment forbidding the Drug Enforcement Administration from undermining state medical marijuana laws, with 219 members voting yes. Also passed were two measures to keep the DEA from interfering with state hemp production or research programs.

What’s making marijuana one of the few issues Democrats and Republicans can agree on? At least as far as the banking amendment, it’s partly about public safety and transparency.

In this year’s guidance to financial institutions, the Financial Crimes Enforcement Network (“FinCEN”) in coordination with the U.S. Department of Justice (DOJ) issued guidelines that clarified customer due diligence expectations and reporting requirements for financial institutions seeking to provide services to marijuana businesses. FinCEN Director Jennifer Shasky Calvery declared that “Our guidance provides financial institutions with clarity on what they must do if they are going to provide financial services to marijuana businesses and what reporting will assist law enforcement.”

At the August, 2014 Mid-Atlantic AML Conference in Washington, DC, FinCEN Director Shasky Calvery, remarked that “just because a particular customer may be considered high risk does not mean that it is “unbankable” and it certainly does not make an entire category of customer is “unbankable”. Banks and other financial institutions have the ability to manage high risk customer relationships. It is not the intention of AML (anti-money laundering) regulations to shut legitimate business out of the financial system.”

Since FinCEN’s guidance went into effect in February, 2014, a reported 105 individual financial institutions from states in more than one third of the country engaged in banking relationships with marijuana related businesses. From FinCEN’s perspective, the guidance is having the intended effect. It is facilitating access to financial services, while ensuring that marijuana-related business activity is transparent and the funds are going into financial institutions responsible for implementing appropriate AML safeguards.

The taxation of marijuana production and sale has tempting budgetary implications for Congress and this country. The 2005 Budgetary Implications of Marijuana Prohibition by Jeffrey A. Miron, Visiting Professor of Economics Harvard University, reported that legalization would save $7.7 billion per year in state and federal expenditures on prohibition enforcement and produce tax revenues of at least $2.4 billion annually if marijuana were taxed like most consumer goods. If, however, marijuana were taxed similarly to alcohol or tobacco, it might generate as much as $6.2 billion annually.

According to Gallup 58% of Americans support ending marijuana prohibition, and Colorado and Washington State has already passed historic ballot initiatives to tax and regulate pot. When it comes to marijuana in the United States, it is no longer a question of when, but how it will be legalized.

This week,

This week,