When smaller, less developed countries from around the world need to exchange their currencies into a more utilized and liquid currency, they utilize SDRs (Special Drawing Rights), essentially a basket of currencies. Created by the IMF in 1969 to supplement a shortfall of preferred foreign exchange reserve assets, namely gold and the U.S. dollar, SDRs have evolved to over $200 billion in value.

The SDRs are currently made up of four currencies, the U.S. dollar, the euro, the yen, and the pound. Over the past few years, China has been aggressively bargaining to have its currency, the yuan, included in the SDRs. Such an inclusion is considered a validation by the IMF that a country’s currency is internationally recognized and accepted.

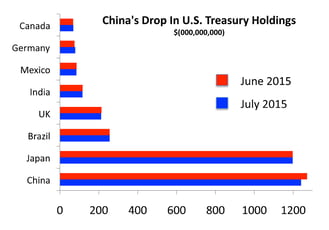

In an effort to strengthen the world’s recognition of its currency, China has entered into currency swap agreements with other countries, bypassing the U.S. dollar as the reserve currency. Currently there are fourteen nations that have signed currency swap agreements with China allowing them to clear their trades using the yuan as the main currency. Those countries include: Argentina, Belarus, Brazil, Canada, ECB, Hong Kong, Iceland, Indonesia, Malaysia, Singapore, South Korea, Thailand, the United Kingdom, and Uzbekistan.

Monday, November 30th

The IMF announced that the Chinese yuan will be included in the SDRs basket of currencies. It is expected that the demand for the yuan will not increase much considering the currency controls of the Chinese government. Central banks have begun acquiring the yuan but they don’t expect to have a major increase in demand.

Central banks don’t use the SDR as a yardstick for determining the composition of their foreign-currency reserves. These are much more heavily influenced by cross-border trade, said Karthik Sankaran, a director of global strategy at Eurasia Group.

Before the currency swap agreements all trading with these countries and China were conducted with U.S. dollars as the reserve currency. While many policy makers don’t believe that the yuan will supplant the U.S. dollar anytime soon, no one thought the Chinese economy would grow to become as big as the U.S. economy anytime soon either.

The inclusion of the yuan in the SDRs Basket is a big deal to China, they view it as placing their currency value equal to that of the other currencies in the Basket. It’s a bit like letting the camel poke its head in the tent! Soon enough the entire camel is in the tent.

In our competitive world economy, China will continue to work at becoming the world’s largest economy and they will compete to become the world’s reserve currency. As the country with the largest population, they want to be a super-power on the world stage and set world economic standards. (Remember they are still a communist nation with limited human rights.)

With the fall of Bretton Woods system and increasing availability of credit through international banking institutions, SDR’s are not used as much as they were when they were first developed. After all we have left the gold standard back in the early 1970’s, which in essence changed precious metals (gold and silver) from a common median of exchange (controlled currency) to a commodity, greatly increasing their value and volatility, particularly as the currencies have been devalued over time.

What are your thoughts of this new development in the world’s economy?

Sources: IMF

Remember

"Peace and contentment come into our hearts when we save a portion of our earnings and avoid unnecessary debt." - Ezra Taft Benson

529 Plans were initially intended to provide parents of young children the ability to save and invest money for future anticipated college related expenses, such as, tuition, books, room and board, lab fees, etc.

529 Plans were initially intended to provide parents of young children the ability to save and invest money for future anticipated college related expenses, such as, tuition, books, room and board, lab fees, etc.

eld bonds, somewhat of an indicator of the credit market’s health. Questionable corporate earnings tend to pull corporate bonds down, feeding into higher stock volatility and price uncertainty.

eld bonds, somewhat of an indicator of the credit market’s health. Questionable corporate earnings tend to pull corporate bonds down, feeding into higher stock volatility and price uncertainty.