Marginal vs. Effective Tax Rates

-

Wendell Brock

- Mar 10

- 2 min read

When people talk about taxes, phrases like “I’m in the 22% bracket” or “I pay about 13% in taxes” often get used interchangeably. But those statements describe two very different concepts: marginal tax rate and effective tax rate. Understanding the difference between them is essential for smarter financial planning, clearer budgeting, and avoiding costly misconceptions about how taxes actually work.

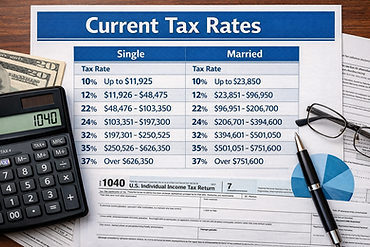

The U.S. tax system is progressive, meaning income is taxed in layers, or brackets. As your income increases, only the portion that falls into a higher bracket is taxed at a higher rate—not your entire income. This is where marginal and effective tax rates come into play.

Your marginal tax rate is the tax rate applied to your last dollar of income. In other words, it’s the rate you’ll pay on your next raise, bonus, or additional income. For example, if you fall into the 22% federal tax bracket, that does not mean all your income is taxed at 22%. It means the top portion of your income, the amount that spills into that bracket is taxed at 22%.

This rate matters most for decision-making. When evaluating whether to take on extra work, sell an investment, or convert retirement assets, your marginal tax rate helps estimate how much of that additional income you’ll actually keep after taxes.

Your effective tax rate, on the other hand, tells a different story. This is your average tax rate across all your taxable income. It’s calculated by dividing the total tax you paid by your total income from all sources. Because income is taxed progressively, your effective rate is almost always lower than your marginal rate.

For example, someone earning $120,000 as a married couple filing jointly might fall into the 22% marginal bracket. However, after accounting for lower brackets and deductions, their effective tax rate could be closer to 13–14%. This number is helpful for understanding your overall tax burden, comparing year-to-year changes, and planning household cash flow.

Confusion between these two rates is common and it often leads to bad financial assumptions. Many people believe that earning more money will push all their income into a higher tax bracket, resulting in less take-home pay. That’s simply not how the system works. Only the income above each threshold is taxed at the higher rate, which means earning more almost always results in more net income, not less.

Deductions can further complicate but improve the picture. Taxpayers can reduce taxable income by choosing between the standard deduction or itemized deductions, whichever is higher. For most people, the standard deduction makes sense because it’s simple and generous. For others especially homeowners, high charitable givers, or those with large medical expenses itemizing may lower their tax bill even more.

The key takeaway is this: your marginal tax rate affects future decisions, while your effective tax rate reflects reality. One tells you what happens to the next dollar you earn; the other tells you how much you actually paid overall.

Understanding the difference helps you make better choices, avoid unnecessary fear around tax brackets, and plan with confidence. Taxes may be complicated but knowing how these two rates work puts you firmly back in control of the conversation and your financial strategy.