Ugh, Taxes!

-

Wendell Brock

- Jul 23, 2021

- 2 min read

Nobody likes to pay taxes. For a lot of us when taxes are mentioned we picture something like the rotten Sheriff of Nottingham collecting taxes from the poor people and whistling happily as he does. We may not have some grabby tax collector knocking down our doors, but the ease of modern online filing and auto withholdings doesn’t remove the sting out of paying taxes. In fact, the burden of paying taxes has been felt since at least 3000 B.C. Taxes have been a part of economies from the beginning.

In 1913 the sixteenth amendment was passed in the United States allowing the U.S. government the power to tax our income. That being said, income taxes are a huge part of our current economy. Our tax dollars fund things like government operations, public services, public spaces and roads, the military, providing assistance for low-income families, and help with national disasters.

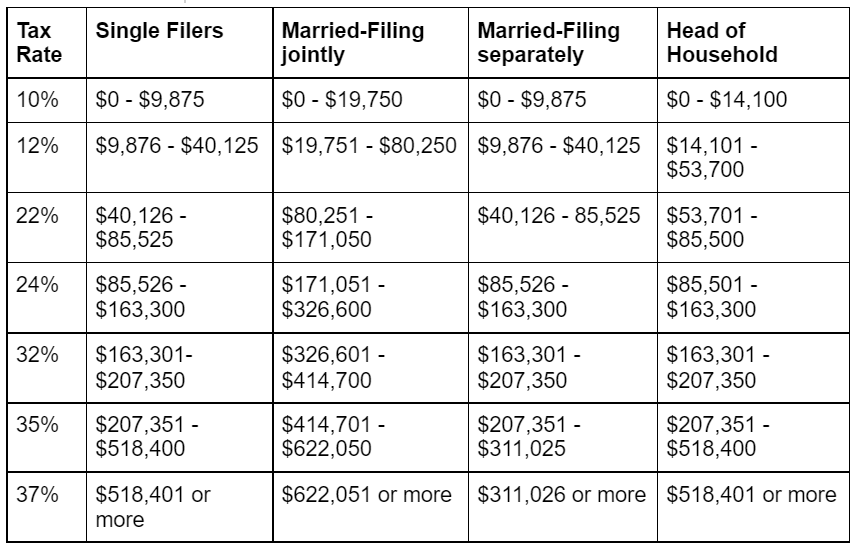

Income taxes in the United States are determined by how much an individual earns, the more you make the higher percentage of taxes you will pay. This encompasses all of an individual's earnings including capital gains. For federal income taxes, the percentage is based on which “bracket” you fall into. This also changes based on how you are filing- single, married: filing separately, married: filing jointly, and head of household.

2020 Tax Brackets

By law, taxpayers must file an annual tax return to make sure all tax obligations have been met. Most employers withhold the appropriate taxes from your paycheck and send them off to their proper places- either the State or Federal government. When you first start with an employer you fill out a W-4 form. This form determines how much of your earnings are withheld. However, this amount is not always perfectly accurate. You may owe more or less. When you file your tax return you get an accurate sum of your income and the taxes due. Often tax liability can be reduced by claiming certain tax deductions. This could result in the government owing you and sending you a refund - this is usually the part people do like.

There are three ways of filing your taxes. You can mail in a form 1040, you can file electronically via tax software. Many people prefer to hire a tax professional that knows the tax laws and can find places to reduce tax obligation.

Working with a financial planner can help you make sense of not just your taxes, but all other aspects of your finances. If you have questions send them our way - questions@yieldfa.com

“There is nothing sinister in so arranging one’s affairs as to keep taxes as low as possible.”

-Judge Learned Hand pg. 134 The Maxims of Wall Street by Mark Skousen