Falling Labor Productivity

-

Wendell Brock

- Sep 23, 2022

- 2 min read

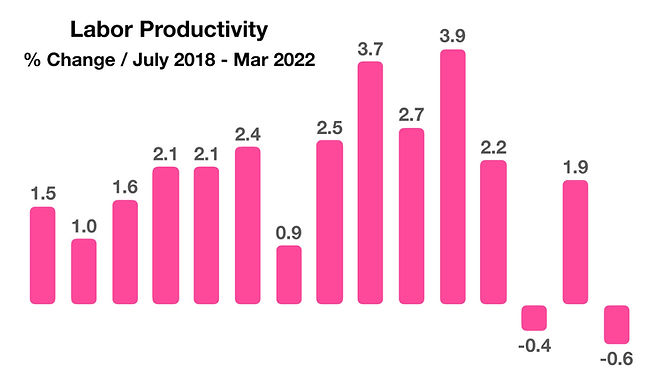

The most recent data released by the Labor Department revealed the largest quarterly drop in productivity since 1947, decreasing at an annualized rate of 7.5%. The drop in productivity was concurrent with the largest rise (11.6%) in labor costs since 1982. Both of these measures are also indicators of inflationary pressures for both companies and consumers. Many companies have been passing along higher costs to consumers, raising prices across the country faster than they have in the last 40 years. Eventually prices will be forced to level out because of competition between companies which will hold prices steady which will require these companies to absorb the higher costs. This could lead to decreased levels of hiring and lower wages as companies struggle to maintain profitability levels.

Data surrounding labor during the pandemic has been considered unreliable and inconsistent by many economists, meaning that the true effects of the COVID-19 pandemic and worker retention are still not certain. An essential data set is labor productivity, which is a measure of how efficiently companies are utilizing workers to produce products and services. This year, the largest four-quarter drop in labor productivity was observed since the fourth quarter of 1993 according to the Bureau of Labor Statistics, marking a historic decline in productivity. Another Labor Department report showed that jobless claims increased to 200,000 at the end of April, the overall number falling to 1.38 million, the lowest level since January of 1970.

Federal Reserve survey results, reported in the Fed’s Beige Book, have identified that a growing number of manufacturers and industrial companies are

increasingly moving towards automation, replacing previously desired workers with robotic gear. Rising wages and a dwindling labor pool have forced some companies to resort to machines instead of hiring workers.